Ho Hum Housing Data In March Provides Hints Of Coming Strength In Spring

Recent signs show housing activity will strengthen meaningfully in April.

The Canadian Real Estate Association (CREA) announced today that national home sales for March were roughly flat, while new listings fell and prices stagnated. CREA analysts are confident that recent activity will harken stronger housing markets for the rest of this year.

There is significant pent-up demand for housing owing to rapid population growth and first-time homebuyers’ fears that prices will rise sharply once the Bank of Canada cuts interest rates. Moreover, Ottawa has been handing out goodies for first-time buyers–leaking what’s to come in the April 16 federal budget. The Finance Minister has already announced the resumption of 30-year amortization on insured mortgages for first-time buyers of new construction. While this is less than meets the eye, in that pre-sales typically require a 20% deposit, the homebuilders’ association is pretty excited.

In addition, Ottawa has eased restrictions on the RRSP Home Buyers’ Plan, allowing F-T buyers to withdraw $60,000–up from $ 35,000 (never mind that the $35K ceiling is hardly ever broached)–with 5 years until repayments must begin, up from two years.

Ottawa is also providing assistance to at-risk homeowners, telling lenders to work with these households to lower payments “to a number they can afford, for as long as they need to” by allowing longer remaining amortizations. The Department of Finance is encouraging lenders to begin working with these at-risk households two years before scheduled renewals. The unintended consequences of this could be significant. For example, what happens to the mortgage-backed securities market and other investors in mortgages? Also, this reduces competition by discouraging refinancings and could raise the cost of borrowing for all participants.

Ottawa has never been very good at considering the second-order effects of their actions. A case in point is the decision to markedly increase immigration (for lots of good reasons) without considering where all of these new people would live. This has led to a massive housing shortage and the least affordable housing in Canadian history. Now that Trudeau’s approval ratings have suffered, they are scrambling to remediate, but increasing demand for housing is obviously not the answer.

There will be more news on Tuesday when I dissect the federal budget’s housing initiatives. The more government money spent, the more money borrowed, which will only raise interest rates from what they will otherwise be.

Back to the March data, national home sales edged up a mere 0.5% month-over-month, although activity rose 1.7%. That was a much smaller gain than those recorded in the previous two months, although a part of that does reflect a mostly inactive market during the Easter long weekend.

New Listings

The number of newly listed homes declined by 1.6% month-over-month in March. “While the official March monthly numbers were quite flat, anecdotal evidence from late last month and early April suggests activity is ramping up,” said Larry Cerqua, Chair of CREA.

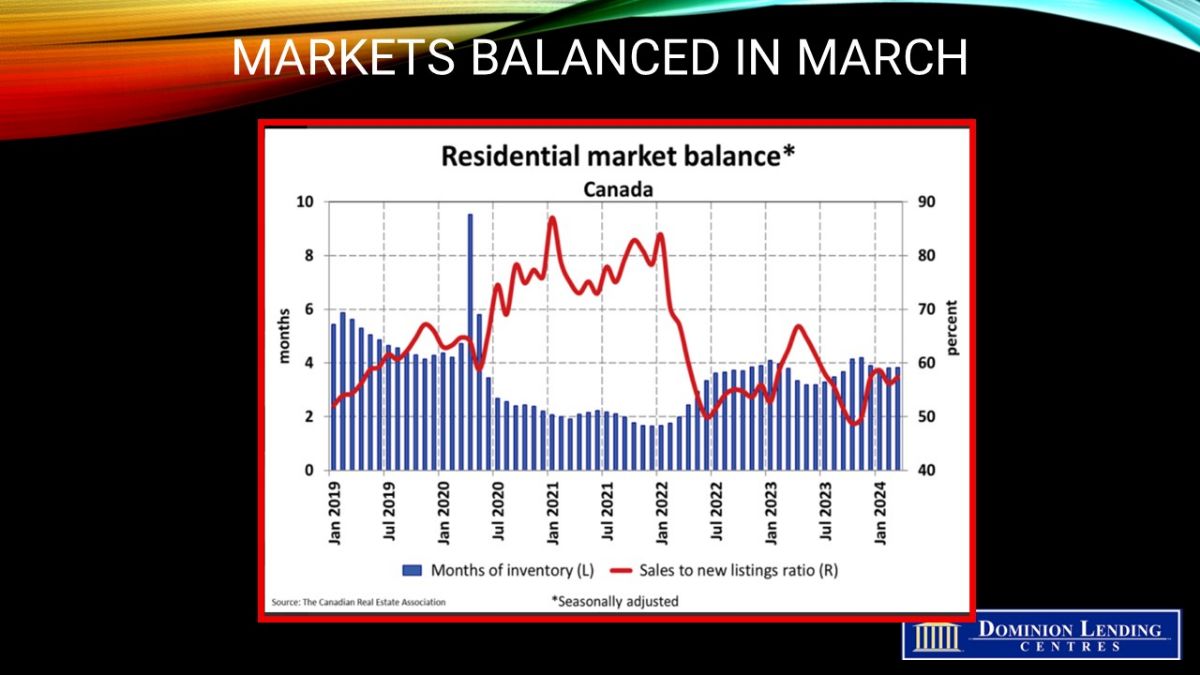

With sales edging up and new listings falling in March, the national sales-to-new listings ratio tightened to 57.4%. The long-term average is 55%. A sales-to-new listings ratio between 45% and 65% is generally consistent with balanced housing market conditions, with readings above and below this range indicating sellers’ and buyers’ markets, respectively.

At the end of March, there were 3.8 months of inventory nationwide, unchanged from the end of February. The long-term average is about five months of inventory.

New listings rose sharply in late March and early April–good news on all fronts.

The actual national average home price in March was up 2% year-over-year from a markedly depressed level. The MLS Home Price Index was roughly unchanged, down markedly from its early 2022 peak when the central bank’s overnight policy rate was a mere 25 basis points before they started hiking rates in March, two years ago.

Bottom Line

With pent-up demand for housing rising with every rent increase, the spring housing season is likely to be robust, even before the central bank cuts interest rates. We believe the BoC will begin reducing the policy rate in June or July, depending on the next two CPI reports. March inflation data will be released on Tuesday (a big day for economic news), and April data will come out on May 21st. The next Bank of Canada decision date is June 5th.

Published by Sherry Cooper

Please Note: The source of this article is from Sherry Cooper

Have questions? Give us a call and we’ll be happy to walk you through the home-buying process.

{kind=link}

{kind=link}